March 2026 Market Updates + Recap

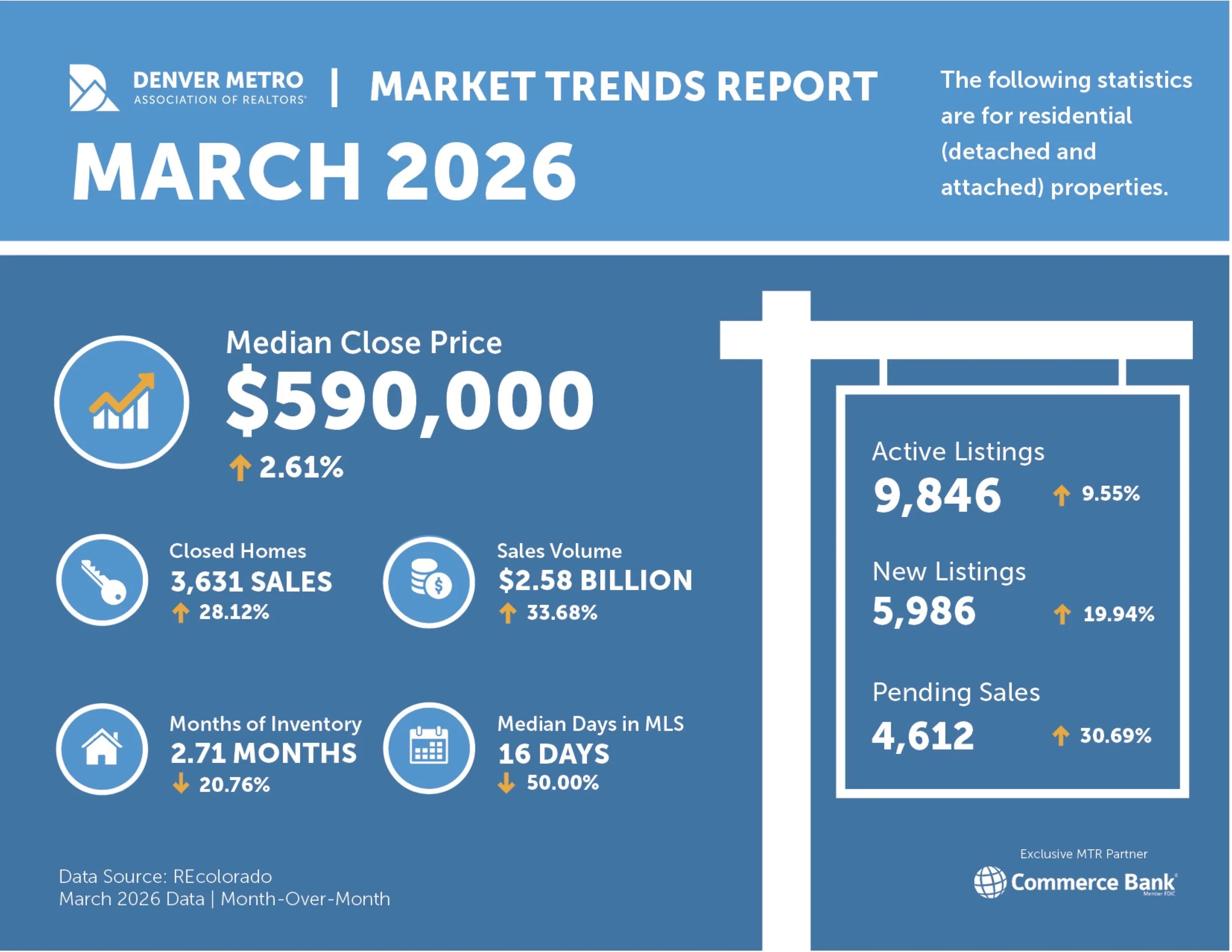

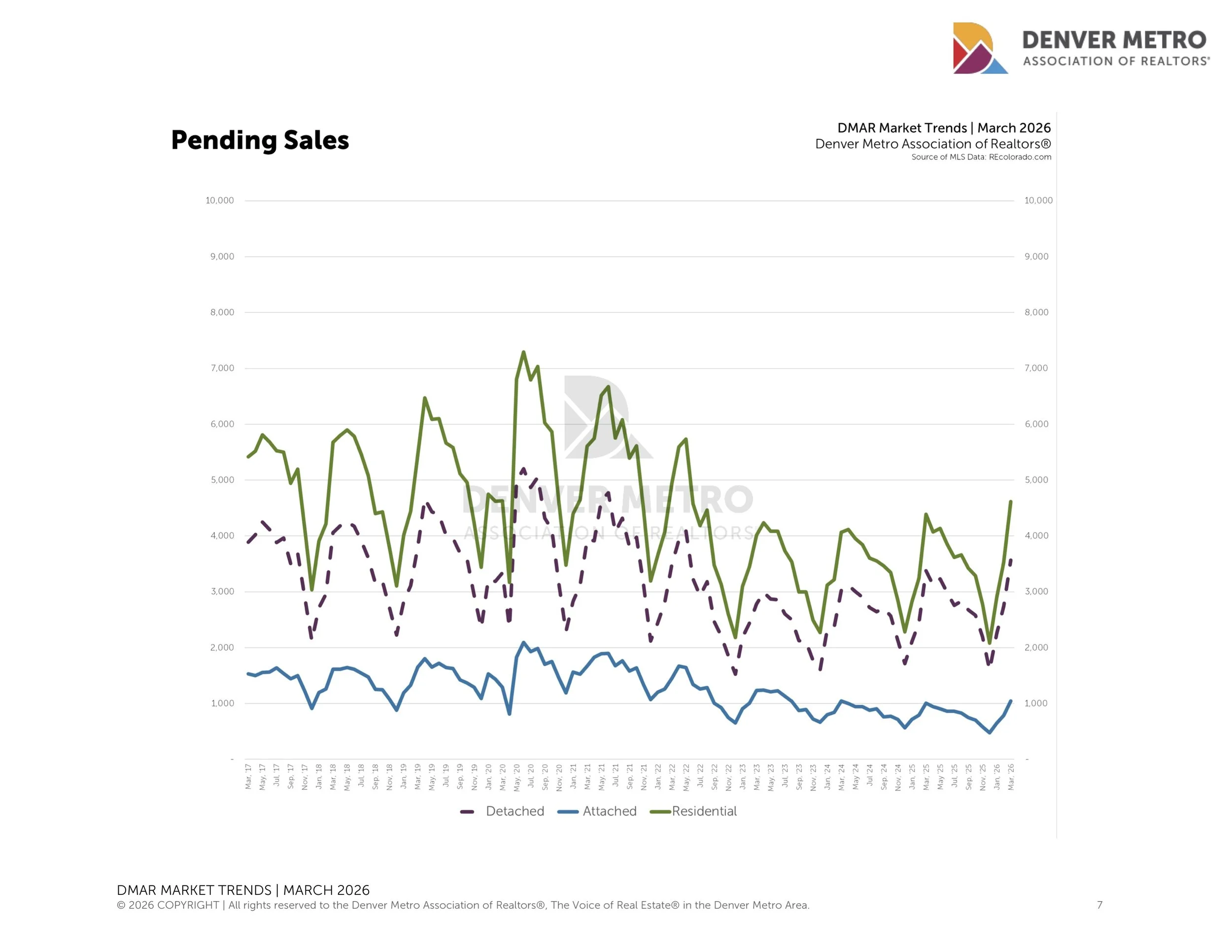

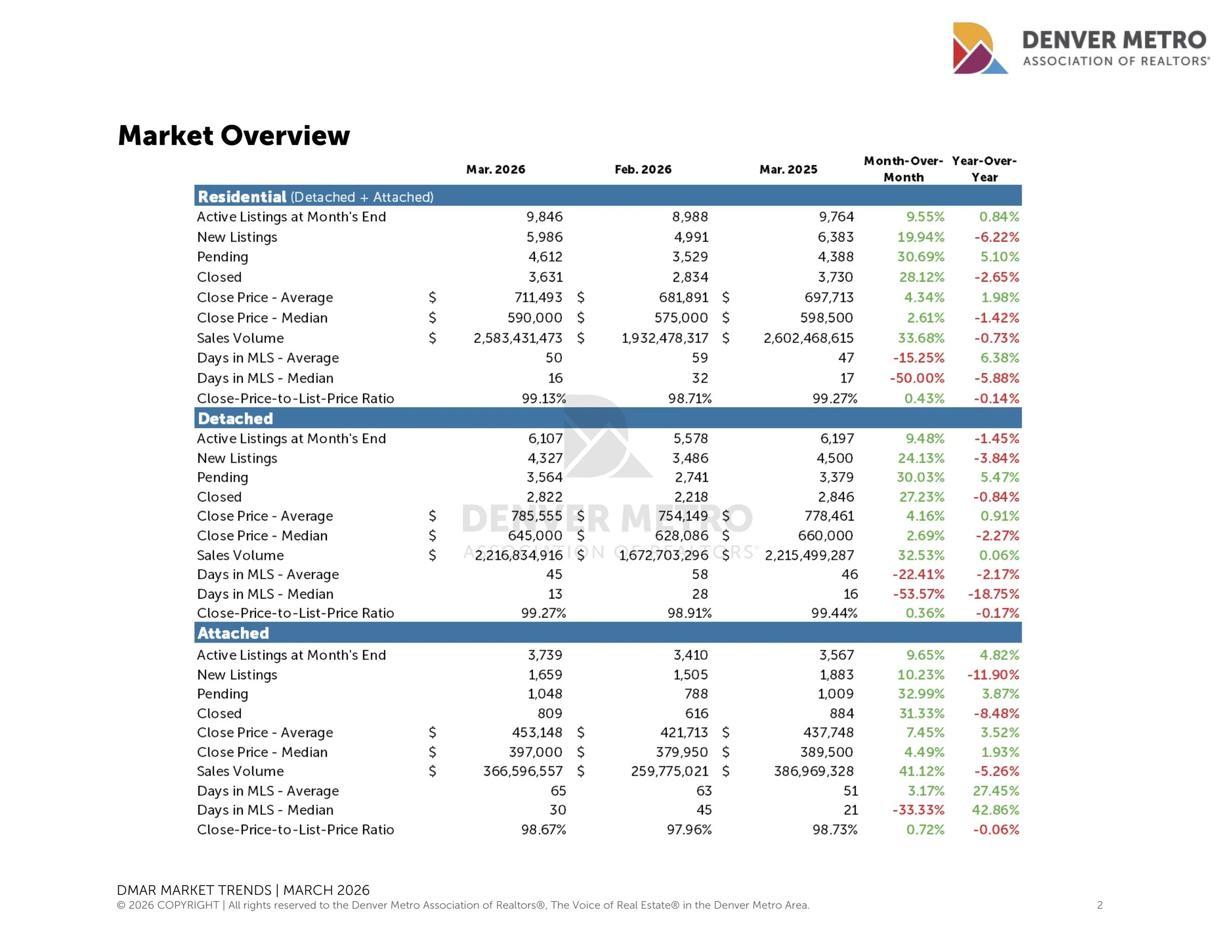

March 2026 reminded us to expect the unexpected, but this time, the unexpected leaned in a positive direction. In this unpredictable environment, the buyers and sellers who showed up prepared were rewarded. The market backdrop remained complicated. Rates climbed back above 6% throughout the month, geopolitical uncertainty rattled financial markets, and new inventory increased nearly 20% from February. Buyers absorbed the new inventory quickly, and pending sales jumped 30% month-over-month.

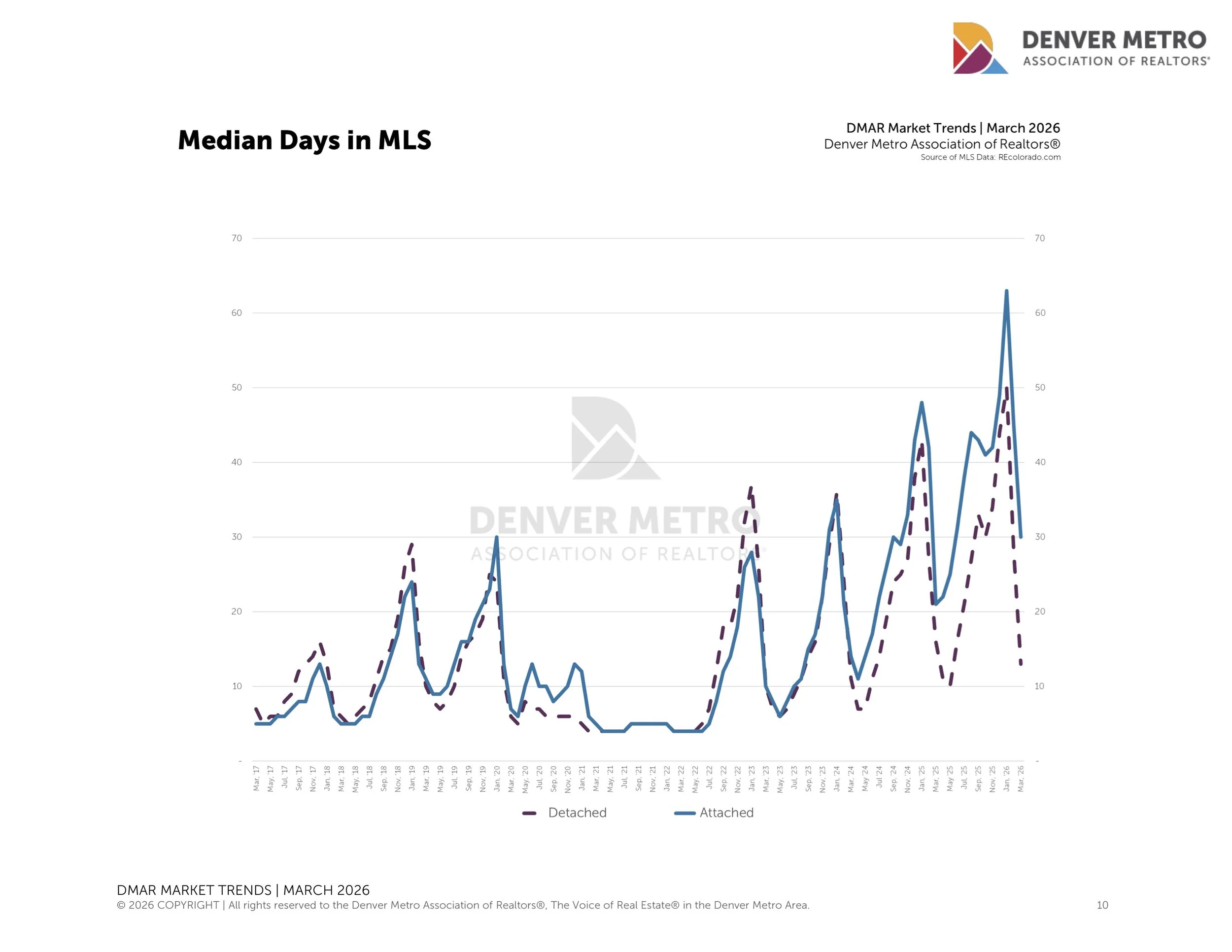

Both detached and attached buyers made decisions with purpose. Detached pending sales were up 30%, and attached were up 33% month-over-month. The close-price-to-list price ratio ticked up to 99%, and well-priced homes in desirable locations saw multiple offers. Days in the MLS dropped 50% month-over-month to just 16 days, showing us that buyers were not just browsing, they were buying.

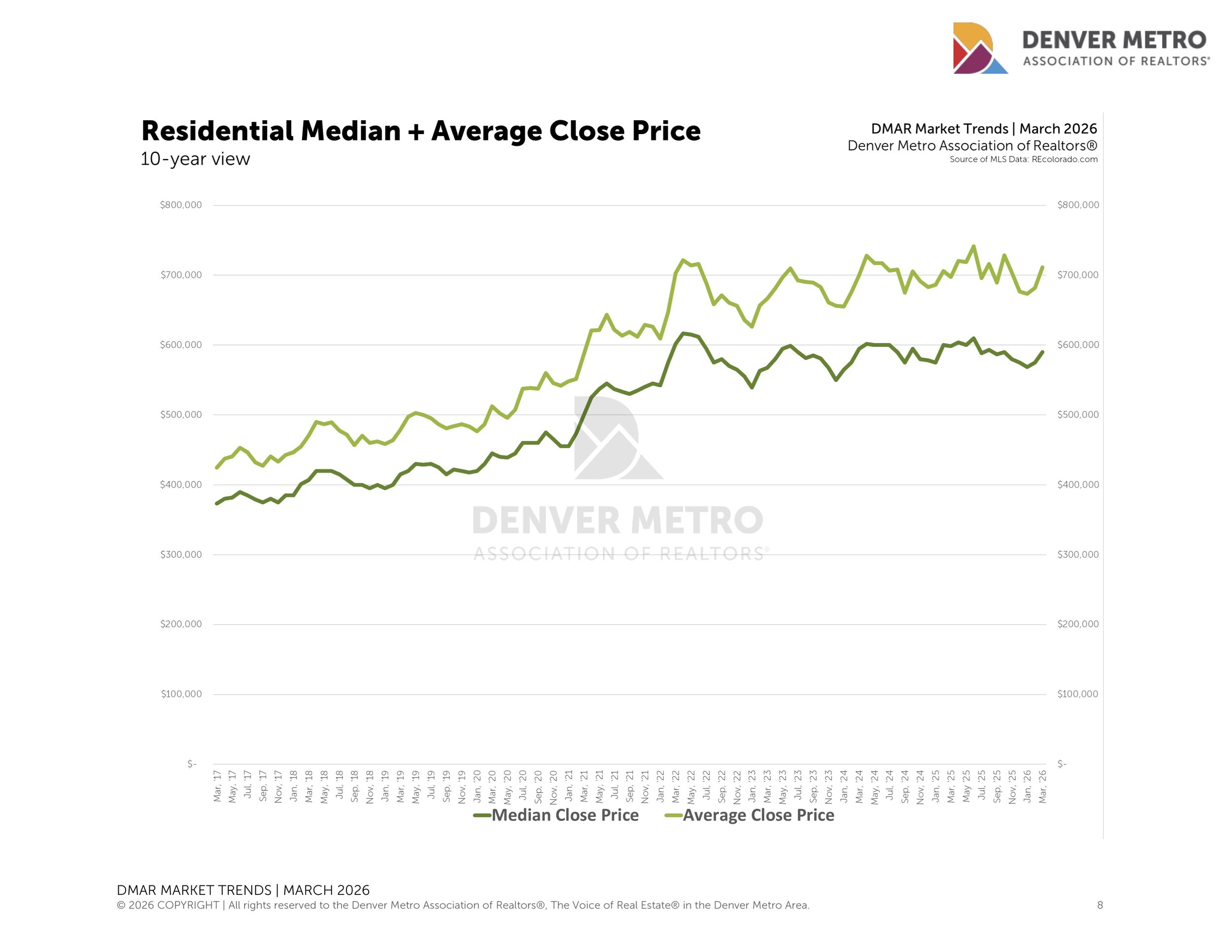

Closed prices reflected the renewed energy in the market. The median close price was up 2.61% month-over-month to $590,000, while the average close price increased 4.34% to $711,493.

Active inventory ended the month at 9,846, up over 9% from February but nearly flat year-over-year. Despite the narrative of more inventory, supply is not dramatically higher than a year ago. The real story is that demand softened over the past two years while inventory normalized.

While the attached market improved in March, the year-over-year numbers tell a different story for condos and townhomes. Closed sales are down 8.48% from March 2025, and median days in the MLS have increased 42.86% year-over-year. Rising HOA fees and insurance costs continue to weigh on buyers in this segment, making accurate pricing and seller concessions particularly important heading into spring.

Year-to-date, 2026 continues to lag behind 2025. Closed sales are down 5.04%, the median close price is down 1.69% to $580,000, and the attached segment remains the softest spot, with year-to-date closings trailing last year by 13.02%.

The buyers who showed up despite rising rates and economic uncertainty validated a market that has been quietly finding its balance. Inventory has normalized, pricing has reset, and demand is returning. The cumulative data may not yet reflect it, but March felt like a turning point. The question heading into April and May is whether the market can sustain it.