May 2026: Market Updates and Review

Real estate feels hard right now. I was chatting with another agent last week, and it’s because no one feels like they have control. It’s making everyone a bit exhausted. Homeownership feels less attainable than ever for buyers, and sellers feel locked in place. Prices are up, and closings are down. How is that possible? Let’s dive in.

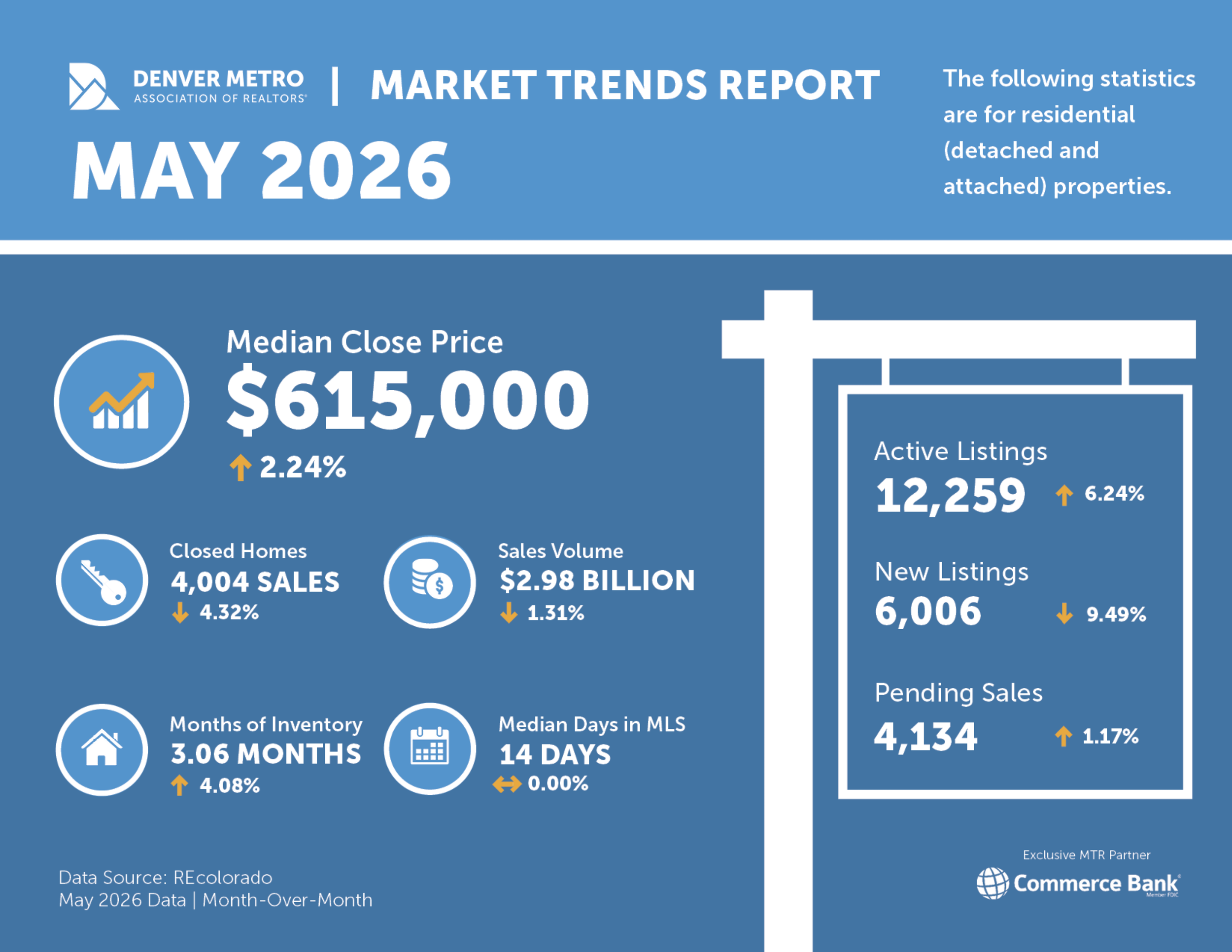

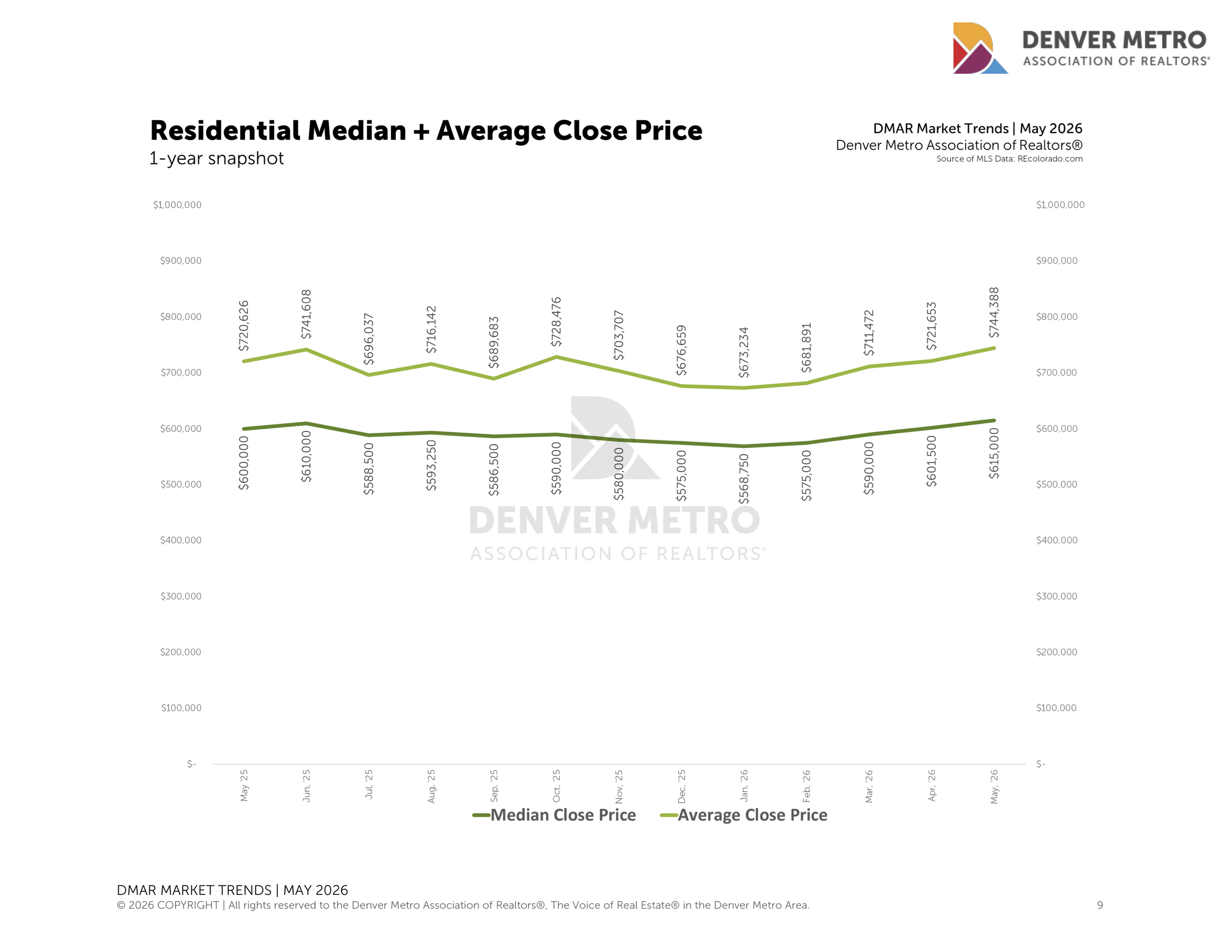

From May 2017 to May 2026, the median sale price grew from $382,000 to $615,000, a 6% average annual increase. The historical norm. In March 2020, a buyer purchasing at the median price of $455,000 with 10% down and a 3.8% rate, their monthly principal and interest payment would be $1,866. If rates remained at 3.8%, normal 6% annual appreciation would bring that payment to approximately $2,580 today.

At 6.5%, the payment on today's median home price of $615,000 is $3,498. That is an 87% increase in six years. The price appreciation accounts for roughly $714 of that monthly difference. The interest rate increase accounts for $918. Interest rates are the affordability problem.

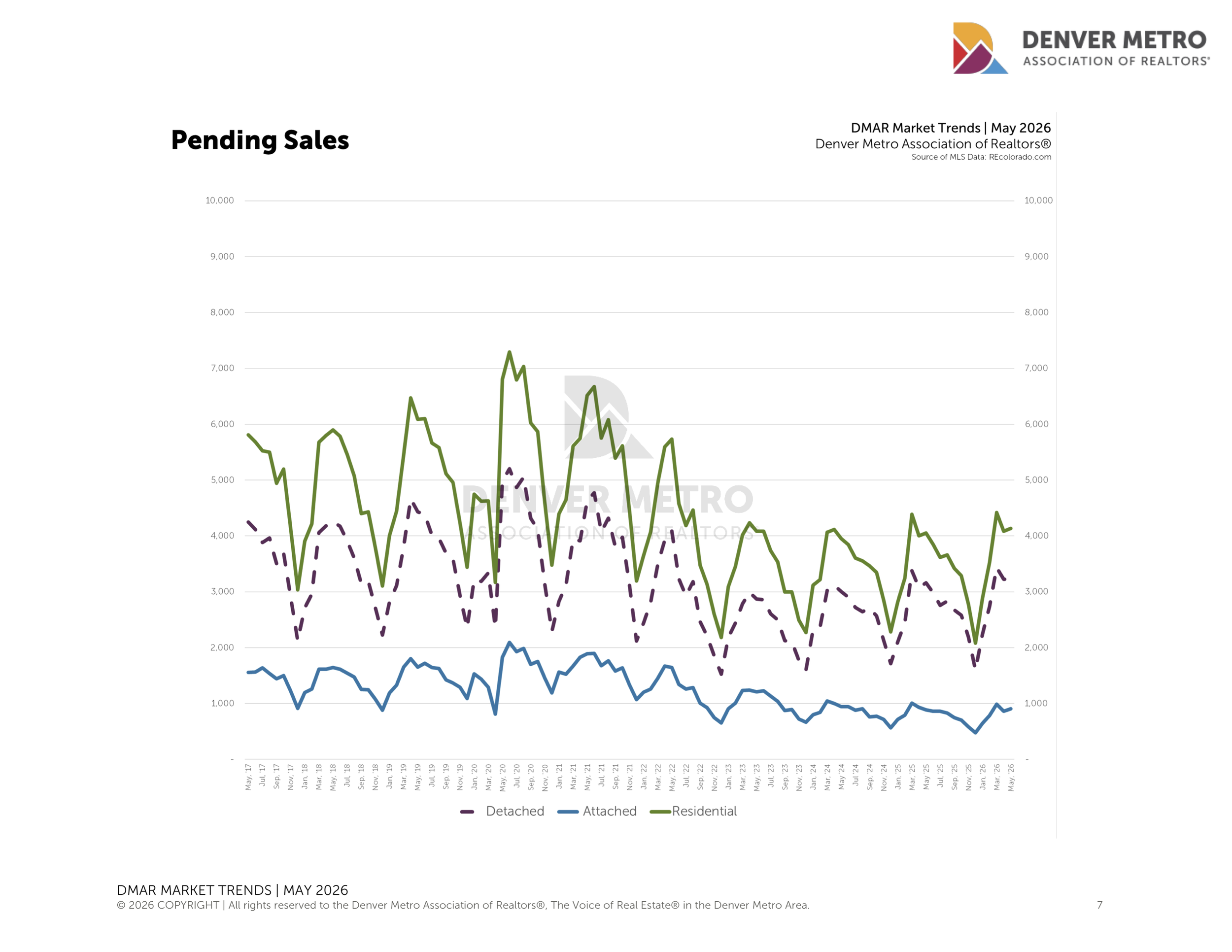

The market is reflecting this reality. Overall, closed sales in May fell 6.97% year-over-year. Attached homes (the market's traditional entry-level product) fell more steeply at 17.84%.

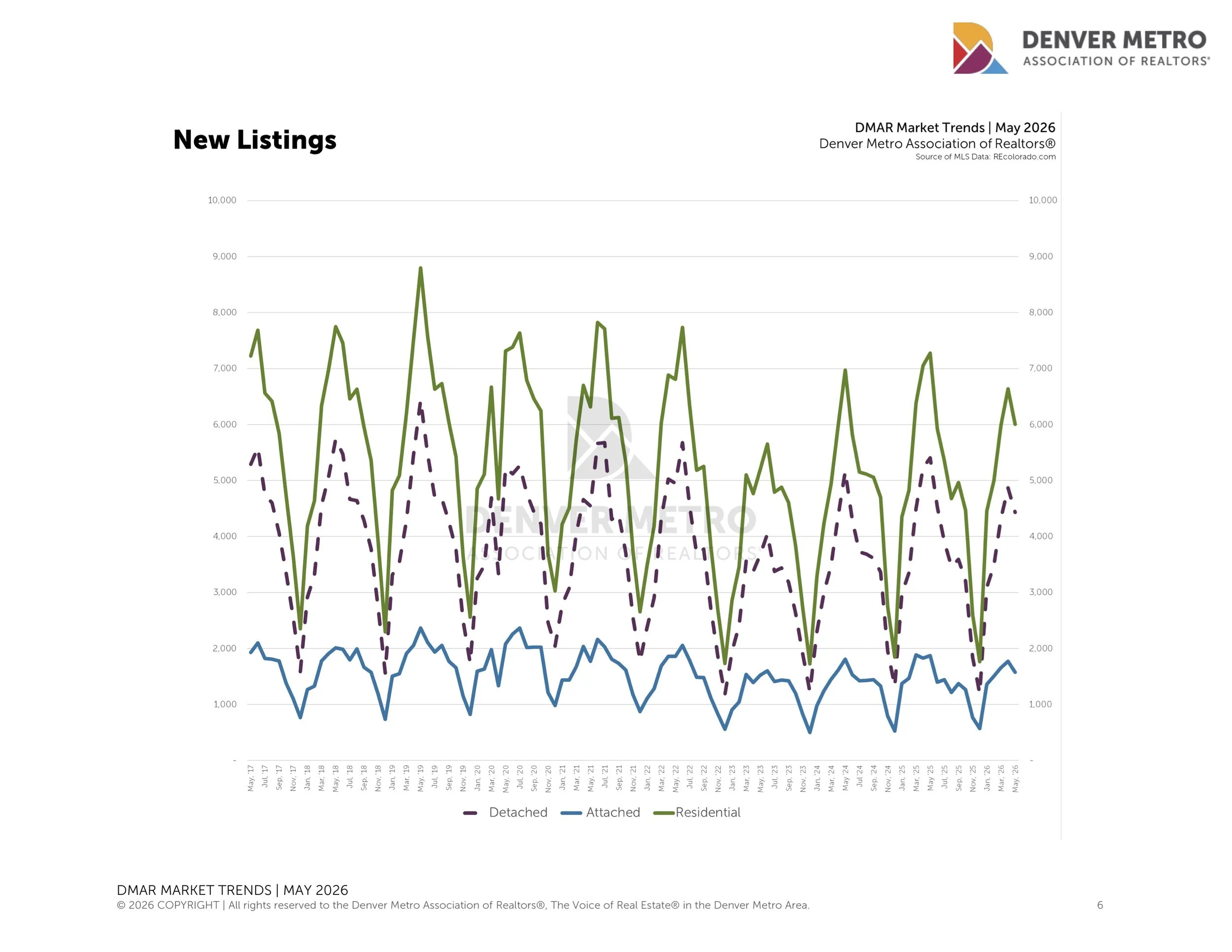

New listings dropped 17.47% year-over-year. Homeowners with 3-4% mortgages face a monthly payment increase of $1,500 to $2,000 on a typical move-up purchase. This is keeping new inventory strained.

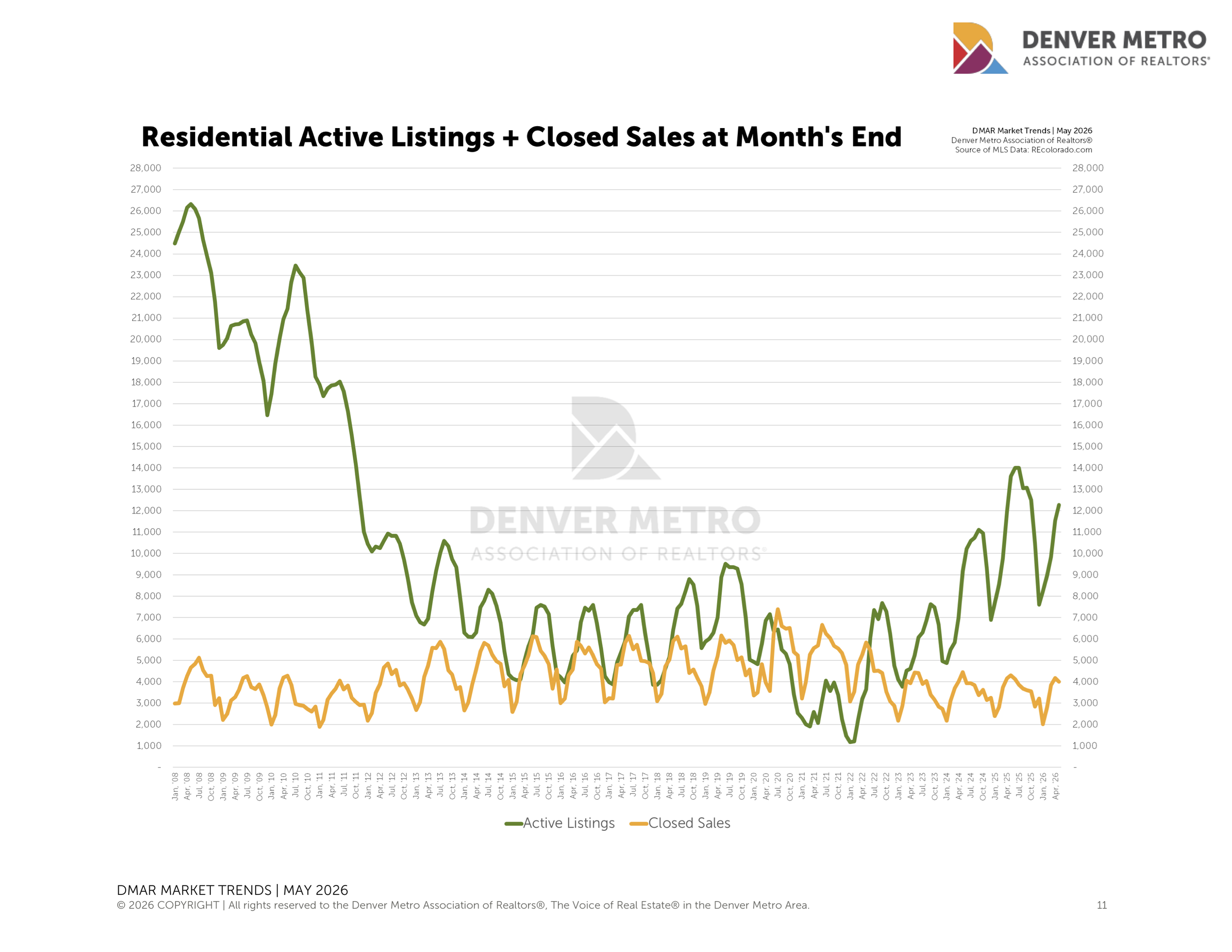

New listings in May were down 9.49% from April, even as the total active inventory at the end of the month grew 6.24% to 12,259. Homes are taking longer to sell, not necessarily representing a surge of new inventory. Inspection contingencies, seller concessions, and rate buydown negotiations are all back on the table.

Buyers in today's market are facing prices that align with the market's long-run historical trajectory, but interest rates are making it feel less so. Focusing on a rate solution is far more productive than waiting for a 40% price correction that isn’t coming. Every 1% decline in mortgage rates reduces the monthly payment on today's median-priced home by approximately $315. I’m negotiating a lot of interest rate buy-downs and getting inspection resolution items fixed for buyers. Sellers want to sell, and buyers want to feel comfortable, so we are finding ways to meet in the middle.

The data shows us that the market is functioning as it should, priced as it has historically been, and made unattainable by forces entirely outside it. The fatigue we are all feeling is a very human response to the unpredictable environment.