April 2026: Market Updates and Review

There was a time when Denver's real estate market (and weather) moved with the seasons. Prices (and temperatures) climbed each spring, peaked between April and June, then eased into fall. That predictability has quietly faded. Over the past three years, the Denver Metro market has settled into something much more consistent and far less dramatic… and much hotter and drier. Let’s get into it!

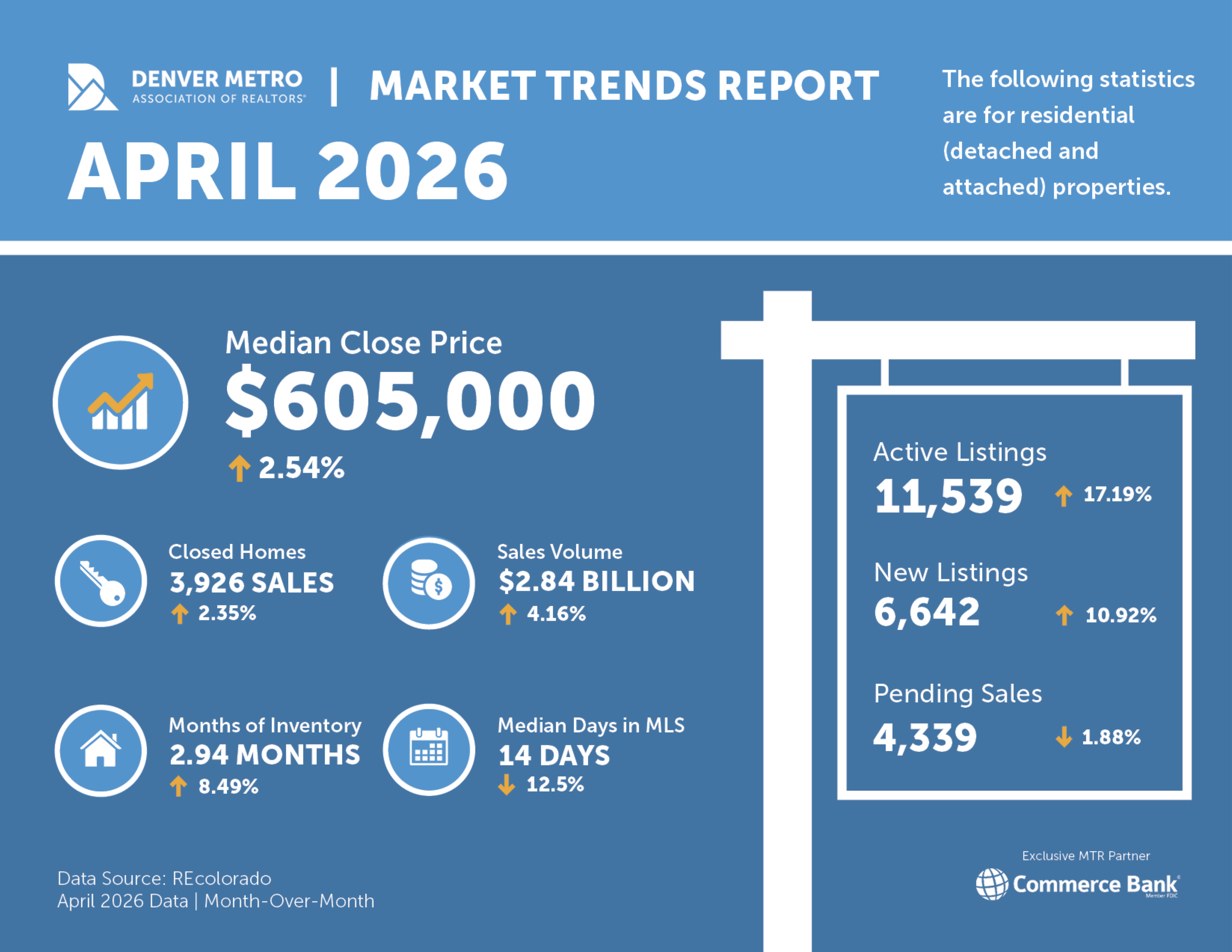

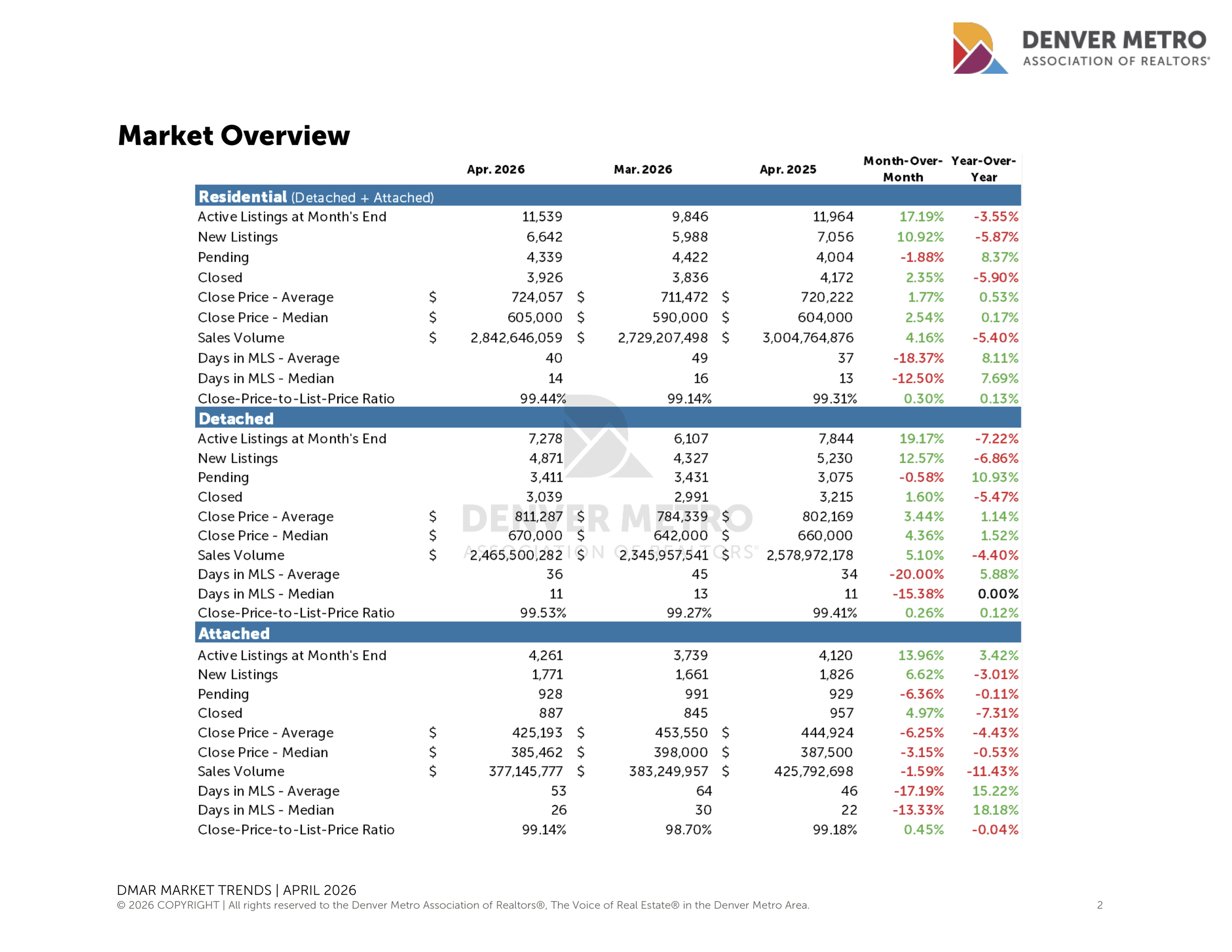

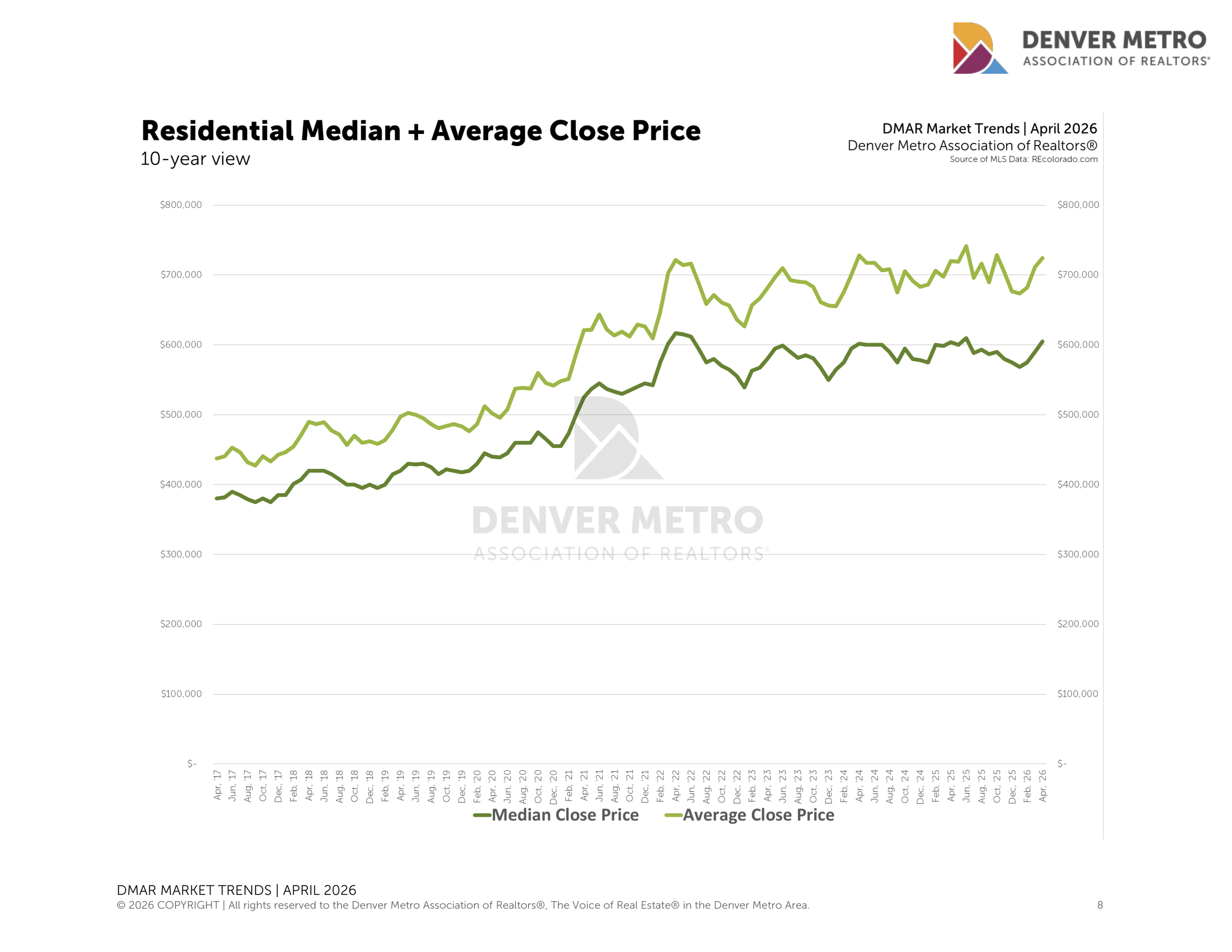

Median sale prices are hovering flat. In April 2026, we saw a median close price of $605,000, in April 2025, it was $604,000, and in April 2024, it was $602,000. Sales volume has followed suit. This isn't a market surging into spring or pulling back into winter. It's a market that has found a tempo of its own, one that is not guided by the human (or weather) behavior of the seasons.

From 2017 through the pandemic boom, Denver's market was defined by its seasonality. Spring brought a reliable surge where buyers competed aggressively, prices jumped, and inventory tightened. The peak years of 2021 and 2022 amplified that pattern to an extreme, with the median sale price rocketing from $473,450 in February 2021 to $616,500 in April 2022, a 30% increase. As mortgage rates rose in the second half of 2022, the seasonal playbook was rewritten and corrected. It was replaced by something quieter and steadier.

April 2026 reflects our new reality. Closed sales came in at 3,926, up 2.35% from March. Year-to-date through April, total closings across the metro area sat at 12,631, down 3.71% from the same period in 2025 and tracking closely with 2024 and 2023. The market isn't contracting dramatically. It's holding its ground in an environment that continually tests its resilience.

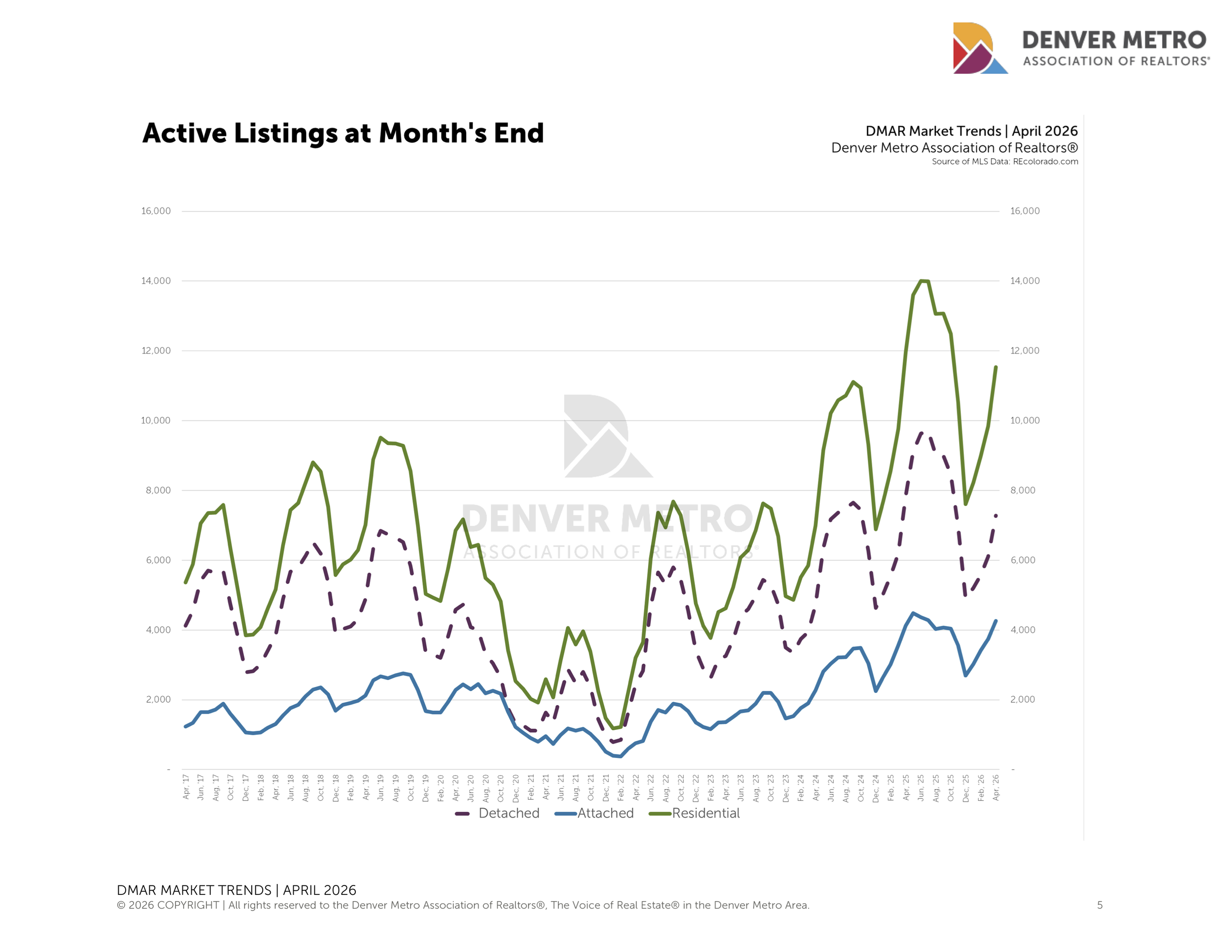

Active listings at month's end reached 11,539, up 17% from March, as sellers continued to enter the market. New listings rose to 6,642, giving buyers a broader selection without oversupply that would pressure prices meaningfully downward.

The average close price of $724,057 similarly reflects stability rather than acceleration, up just 0.53 percent from April 2025. Sellers are still commanding near full ask, with the close-price-to-list- price ratio at 99.44%. This is only slightly higher than a year ago, a signal that well-priced homes are not sitting idle despite the increase in available inventory.

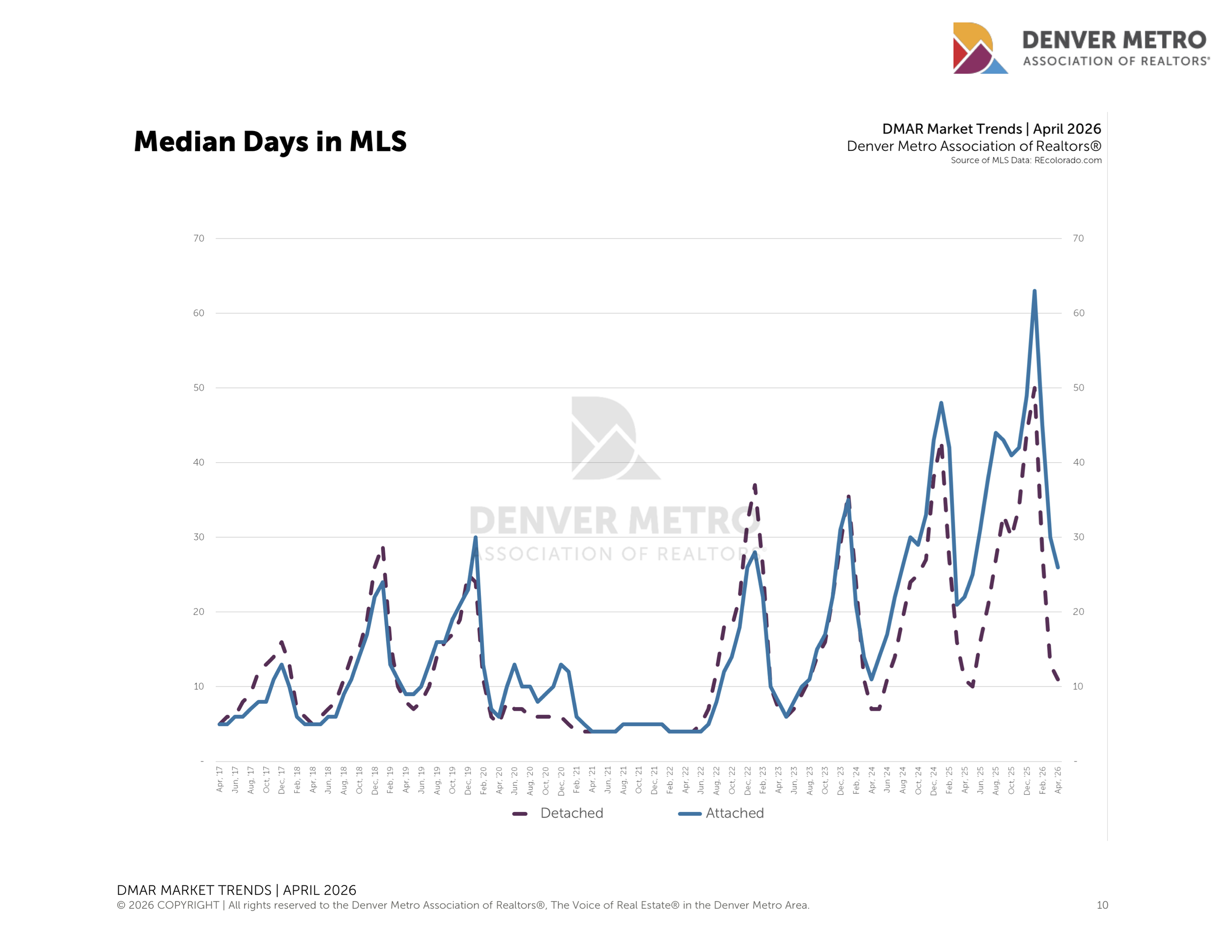

Perhaps the most telling number is days in MLS, which tightened to a median of just 14 days in April, down sharply from 16 in March, and only one day longer than April 2025. The market is moving.

The steadiness continues to be good news for buyers. More inventory means more time to evaluate options, and more options to evaluate. Sellers should resist the temptation to test the market with aspirational pricing. The data is consistent, and buyers know it.